Recent discussions about carbon dioxide removal (CDR) often focus on challenges rather than opportunities. While the Wall Street Journal has described the road ahead as "long and expensive," this framing misses the transformative potential of early market engagement.

The traditional view that companies should only engage with carbon removal as direct compensation for residual emissions overlooks a powerful alternative objective: investing in climate innovation. As demonstrated by forward-thinking companies like Celonis, combining carbon reduction strategies with active investment in innovative removal projects can accelerate global climate action beyond any one organization's value chain.

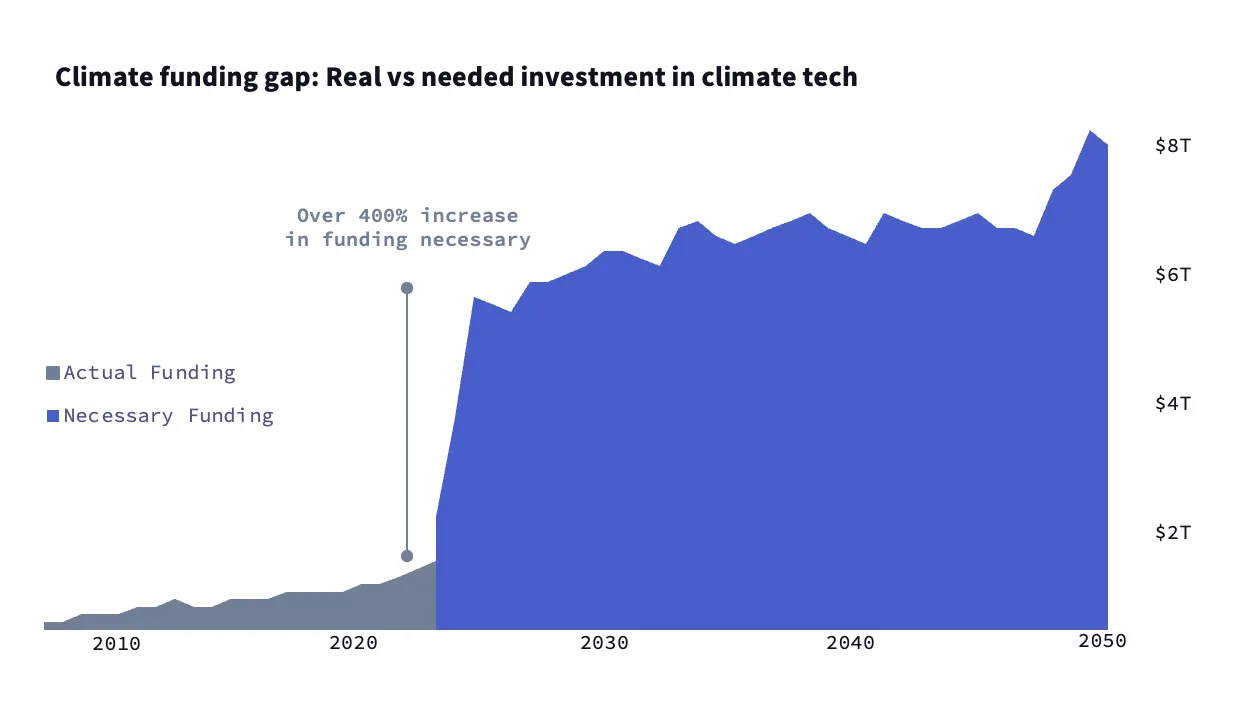

This investment perspective recognizes that CDR isn't just about clearing corporate footprints. It's about catalyzing a vital climate technology that could become a trillion-euro global industry by 2050. CDR isn't a niche solution but an essential component of meeting Paris Agreement targets.

Building the CDR market through early participation

Europe is uniquely positioned to lead in carbon removal with its technological expertise and progressive climate policies. However, bridging the gap from currently capturing 2 million tons of CO2 annually to the 450 million tons needed by 2050 requires immediate action.

The Celonis approach demonstrates how forward purchases — agreements to buy carbon credits before they're generated — provide crucial upfront capital enabling project developers to scale operations and accelerate carbon removal efforts. This model of climate contribution combines both emission reduction and active investment in innovative climate solutions.

First-mover advantages in an emerging market

Organizations that invest early are securing significant advantages through early market engagement:

Strategic access to limited supply

With only 1 million credits issued since 2017 by leading durable CDR registry Puro.earth, early movers are already securing preferential access to high-quality removal credits. High-quality removal projects that can generate secure climate impact at good prices are regularly sold out way before the first issuance (i.e. before the first credits are generated) - only investing early can secure access and volumes.

Financial benefits

Similarly, in terms of locking down better pricing, companies like Zurich Insurance are positioning themselves strategically through forward-purchasing agreements through deals that have "secured credits at prices below where they will potentially trade on a spot basis and include options to purchase further issuances at rates they have already locked in," explained Chris Minter, sustainable supply chain lead at Zurich Insurance Group.

Innovation leadership

The Celonis partnership with CEEZER demonstrates how leading companies can become active participants in scaling climate solutions and are driving the innovative thinking needed to accelerate the development of the voluntary carbon market. This enables companies to extent their climate impact well beyond their own direct (or indirect) footprint by catalyzing the technologies needed for the next centuries.

Science-Based Targets initiative aligning on CDR

The Science Based Targets initiative (SBTi) now recognizes carbon removal as a definitive part of corporate net-zero strategies. Even their most conservative standards acknowledge that beyond-value-chain mitigation through carbon markets and supplier empowerment strategies has become essential for comprehensive climate action — and more so essential to reach net-zero targets in reality.

SBTi's draft Corporate Net-Zero Standard Version 2.0 represents a notable evolution in their approach to climate action. While still maintaining their fundamental emphasis on emissions reductions first and foremost, the new standard outlines three potential options for integrating CDR into a company's net-zero pathways. This marks a measured shift from its previous stance, which effectively limited the role of CDR until the very last stages of decarbonization. This evolution recognizes that without early investment in carbon removal technologies, the necessary CDR capacity simply won't exist when companies reach their net-zero target years.

Importantly, this evolution makes the net-zero standard more achievable and practical for companies that previously struggled to see a viable implementation path. It also addresses a critical market reality: the CDR capacity needed for net-zero targets in 2030 or 2045 cannot materialize overnight. Many stakeholders have rightfully pointed out the contradiction in expecting companies to purchase significant volumes of durable CDR in their target years while discouraging early market participation that would help develop that capacity in the first place.

Why durable CDR matters

While nature-based solutions like reforestation are vital climate tools, they face physical constraints. Land competition, permanence concerns, and verification challenges mean we cannot rely solely on these approaches to deliver the gigaton-scale removal needed.

In the meantime, the economics of CDR are following a predictable pattern we've seen with other climate technologies. While they currently can be 10-fold the price of nature-based removals, prices have been coming down quite consistently across technologies. But for a further price down, more investment is needed to allow for a larger scale. This is where early buyers can make a huge difference by investing early. We have seen this happening with many For example, where solar power was once prohibitively expensive, it has become one of our cheapest energy sources through early investment and deployment.

Build your own strategic CDR portfolio

Early engagement with CDR doesn't mean rushing in without a plan. Building a diversified CDR portfolio should factor in both time horizons and technology types, balancing near-term investments in more affordable solutions like biochar with smaller allocations to emerging technologies like DAC that offer greater durability.

Your optimal strategy will depend on where emissions occur in your value chain as well as their chemical nature. Analysis shows that for most industry sectors with fossil emissions, implementing carbon capture and storage (CCS) is currently more economical than purchasing carbon removal credits. However, CDR prices are projected to decrease significantly, eventually making them more cost-effective than in-house carbon capture for many industries by 2036. (Learn more in our white paper: Creating Value With Green Carbon: CCS and CDR as Complementary Measures for Decarbonization.)

Crucially, your CDR approach should complement — never substitute — ambitious internal emissions reductions and be integrated into your existing supply chain. To that end, companies should begin assessment and planning now, even if large-scale implementation comes later. Understanding your emissions profile, evaluating technological fits, and monitoring market developments costs relatively little but creates substantial option value.

Partners like CEEZER can help de-risk these investments through in-depth project data, live monitoring, reporting and verification (MRV) on project progress, and comprehensive due diligence that provides transparency throughout the carbon removal journey.

Reframing CDR as a strategic investment

Rather than seeing the challenges of scaling durable carbon removal as reasons to delay, forward-thinking organizations recognize them as opportunities to lead in climate innovation.

For companies ready to begin their CDR journey, partners like CEEZER can provide critical support with long-term offtake agreements, expertise in navigating the complex removal landscape, conducting due diligence on projects, and structuring forward purchases to help your organization secure future capacity while managing risks.