.webp)

The voluntary carbon market looked and felt shaky in 2024. Issuance volumes dropped by around 17 percent and corporate climate ambition felt stalled. But zoom in and it’s clear: This market isn’t collapsing, it’s evolving.

What we can see is corporate sustainability leaders stepping up their game quietly, but effectively. The value of retired credits increased 29 percent, buyers engaged with sophistication and most notably, a decisive shift toward carbon dioxide removal (CDR) has hit the mainstream.

Today the question is no longer whether to engage, but how to make the most of it. With removal credit prices reaching approximately $20 per ton and avoidance credits continuing their steady decline, the market is sending clear signals about where value lies.

Four key factors emerged in 2024 and will fuel growth in 2025. Here, I share what you need to know and how best to participate within them.

1. Stable volumes, higher value

The voluntary carbon market's apparent paradox — declining issuance volumes on one side, rising retirement values on the other — tells a real-time story about market maturation. Our data suggests the estimated retirement value climbed 31 percent to $992 million year to date in 2024, while new issuance volumes fell 21 percent to 309 million tons.

This isn't a contradiction. It’s a clear signal of a market recalibrating around quality and impact. Two key metrics illuminate this transition:

Widening value gap

Additionally, the price gap between removals and avoidance credits is widening. While removal credit prices have held steady at around $21 per tonne and rose from December 2023, avoidance credit prices have declined to less than $4 per tonne in November 2024 from more than $9 in February 2023. This spreading gap reflects a fundamental market repricing of different credit qualities and kinds of impacts.

Average portfolio expansion

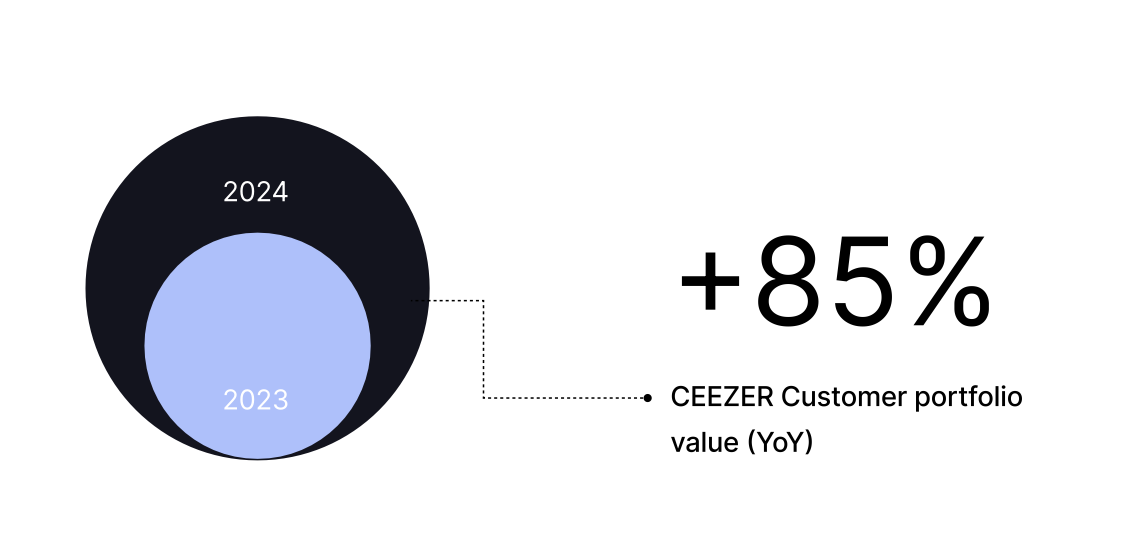

We see buyers shifting from opportunistic purchasing to strategic portfolio building. This approach typically combines high-quality avoidance credits for immediate impact with multi-year removal credits for long-term climate goals, driving up overall portfolio values even as volumes moderate.

On the CEEZER platform more specifically, we have seen a 85 percent expansion of average yearly portfolio value for existing partners. This means buyers are investing more per ton in order to create portfolios that are ready for net zero.

Portfolio composition is evolving

The evolution of carbon portfolio strategies in 2024 reflects a growing sophistication among market participants as more companies increasingly adopt 3- to 5-year horizons for credit procurement, moving away from ad-hoc purchasing.

We also see increased demand for risk diversification, with buyers moving to hedge their investments strategically across various technologies and geographies to mitigate potential risks. Buyers too are seeking a balanced approach with carbon portfolios commonly featuring a mix of removal and avoidance credits aligned with both immediate and long-term climate goals — all of which requires enhanced due diligence built on a thorough assessment of project quality, permanence and co-benefits.

What this means for 2025:

- Differentiation between removal and avoidance credits will likely continue to drive prices.

- High-quality credits, particularly those with strong removal components or exceptional co-benefits, will command premium prices and require early commitment from buyers to keep supply available.

- This trend suggests a market that increasingly rewards quality over quantity. With overall issuance volumes slowing in lower-price, lower quality categories, buyers are increasingly competing for a relatively small pool of high-quality credits.

What this means for your company:

- The optimal time to build a diversified portfolio for the long term is now.

- Securing technologically mature removal credits for multiple years ahead can lead to price and volume advantages .

- Sound understanding of current and future quality, price, and volume risks required to be successful.

2. The shift towards carbon removal continues

In line with evolving portfolio composition, growth in the carbon market has come primarily from carbon removal, with prices across categories rising in recent months.

A premium of future vintages

In some categories, especially nature-based removals, data from forward listings shows that premiums are increasingly priced into future credit volumes. Suppliers of well-rated, high-quality projects with strong digital monitoring abilities are starting to offer, and sell, future vintages at a premium, rather than a discount, as there is a clear expectation around increasing prices. This means that some long-term offtakes will deliver a reduced price increase, rather than a price discount. Meanwhile, sought-after projects are selling out ahead of issuance and increasingly are setting the terms for buyers to engage in the long term.

Continued surge in permanent CDR sales

Permanent CDR sales surged once again by a multiple, growing an estimated 300 percent YoY in purchased tons. Permanent removals are small in comparison to the remainder of the market but are by far the fastest-growing segment. Much to the benefit to the market, the average value did not grow as quickly (“only” by 106 percent), indicating that the price for permanent removals continues to decline as technologies mature and plants leave the pilot stage.

This is another sign of maturation, as new permanent technologies become more accessible to buyers. Notably, BECCs credits took a significant share of CDR sales this year so far, from much less volume in the previous years.

What this means for 2025:

- Emphasis on removal credits in corporate portfolios will continue to increase.

- More accessible removal categories (for example, nature-based solutions) will require long-term contracts with already planned price increases.

- More expensive, technological removal categories will continue to come down as technologies scale and available supply grows.

What this means for your company:

- Investing in more accessible, high-quality removal credits <$50 per tonne will require longer-term commitments with the ability to reduce price risk if done soon.

- Companies require increasing expert guidance and tooling to access the global network of high-quality projects and unlock volume.

- An in-depth understanding of quality, policy, price and volume risk will be paramount to balance risk and reward.

- Securing already scalable permanent CDR solutions today can help reduce delivery risk in the future.

3. A widening buyer base

The carbon market's continued expansion is reflected in its diverse participant base, with an estimated 5,000 unique buyers worldwide in 2024. This broadening engagement reveals important shifts in both who's buying credits and where investments are flowing. Key sectors are emerging as market drivers, with energy, telecommunications and professional services sectors leading retirement volumes.

The broadening participation base suggests that despite less volume growth than in previous years, the long-missing part of the market (diverse buyers) is evolving for the better. Moreover, it shows enterprises are increasingly owning their carbon market engagement, as new tooling and expert support to monitor quality and price risk is becoming available and accessible.

This trend is accelerated by the increasing pressure to decarbonize global supply chains. Many corporations, now well underway on their internal decarbonization path, are shifting focus on their supply chain emissions (commonly referred to as scope 3).

And yet, many companies also report being delayed on their path to scope 3 target achievement, with suppliers often having little incentive to transition for a single buyer or struggling to deliver on promised emission reductions. Supply chain sustainability teams are more and more engaged with suppliers to leverage carbon markets as an additional tool to make up lost time. While the exact applicability of carbon credits differs by framework and is quickly evolving (see below), technologies and tools are now available to make collaboration on carbon investments easy, quick and risk free. Also, companies can offer real value to suppliers by giving easy guidance on portfolio requirements in offering a curated access to the market, leveraged by technology.

What this means for 2025:

- Buyers continue to use new avenues to directly participate in the market - leveraging new services and technologies to effectively balance risk and impact.

- Increasing buyer base will continue to diversify with higher-margin industries increasing share of high-quality removals in their portfolios.

- Collaboration in climate investments will rise as technological solutions are available to reduce transaction and coordination cost.

What this means for your company:

- The tooling and expert advice to directly engage in the VCM is available and ready for buyers across industries, leveraging specialist support can streamline the carbon market journey.

- Direct engagement can be easy across all industries, but companies need to ensure they use all available supporting data to mitigate risks in the market.

- Collaborating with others on carbon investment can help gain economies of scale. Technology can help make that process frictionless, secure and reduce risk.

4. Quality standards and market infrastructure continues to solidify

This year has seen significant progress in strengthening market integrity with the implementation of key frameworks, including the ICVCM's Core Carbon Principles (CCP) and VCMI's Claims Code of Practice. Both are gaining traction, providing clearer guidelines for both buyers and sellers. CCP has quickly become a strong “label” that is used in the market, and the options for external claims guidance have grown.

The question of scope 3 remains open

Earlier this year, many experts anticipated more guidance on whether carbon credits and beyond-value-chain mitigation activities can be counted against scope 3 targets, a crucial question for many practitioners. Mentioning the mere possibility almost led to a dismantling of the leading target framework, the Science-Based Target Initiative, which has been overhauling the widely used corporate net-zero standard for most of the year.

Needless to say, while SBTi published a longer technical report on Scope 3 target achievement best practices, both the net-zero standard and the particular guidance on credit use against scope 3 targets were delayed. VCMI’s claims code of practice, however, offered multiple updates on their claims code of practice and concluded a public consultation on the scope 3 target applicability. The publication of VCMI’s Scope 3 Claim, expected January 2025, might be the first target system under which beyond-value-chain mitigation can be used to count against scope 3 targets under certain circumstances.

Double counting? Addressed. Real impact? Still a work in progress.

COP29 brought progress on the long-expected approach of compliance and voluntary markets via Article 6.4 of the Paris Agreement. Article 6.4 allows for the transfer of credits between private market participants under adjustment of the relevant NDCs.

While the system in itself is not groundbreaking but merely an evolution of the Clean Development Mechanism (CDM) — whose shortcomings were, in many ways, a catalyst for the creation of the VCM — the now-approved Article 6.4 framework promises some progress: mainly, that the inclusion of removal credits is now possible.

This is noteworthy as the UN-sanctioned credit schemes have long suffered from old methodologies and a lack of innovation. Current drafts of Article 6.4 allow for the transfer of older CDM methodologies, which can prevent double counting of mitigation, while still opening the future compliance system to newer methodologies. And yet, what quality and risk requirements must be met to be approved, however, are neither ambitious nor concrete enough to actually ensure quality under Article 6.4.

What this means for 2025:

- We expect further refinement of quality standards and frameworks, with a growing emphasis on transparent reporting and verification for both buyers and sellers.

- With the challenge of scope 3 decarbonization continuing and increasing pressure on scope 3 targets, we expect frameworks and standards to move to a more open stance on allowing market-based instruments to facilitate (partial) target achievement along the value chain.

- Progress under the Paris Agreement will lead to increasing availability of policy-aligned credits that might very well come from existing VCM carbon projects with a Letter of Approval from the host country. These will likely command a higher price but the inclusion in Article 6.4 will not mitigate risks outside of double counting.

What this means for your company:

- The focus on quality and transparency across standards and frameworks necessitates access to real-time, reliable data. CEEZER's MRV Data Integration — partnering with Carbonfuture, Cula, Kanop and Mangrove Systems (with more to come) — positions us to meet this growing need for comprehensive, up-to-date information.

- scope 3 remains a key challenge but early buyers are already including suppliers in their carbon credit portfolio planning. CEEZER’s supplier solutions can help with scalable technology to make co-investing in carbon credits easy.

- Expect paying premiums for credits with an issued Letters of Adjustment under Article 6.4 as supply is still scarce. That said, assessing the specific project risks will remain absolutely necessary as the current processes for Article 6.4 do not ensure credit quality.

A strategic look ahead to 2025

The voluntary carbon market is evolving and maturing, measurably and for the better. Scrutiny has never been higher as the planet, and humanity, cannot afford bad investment.

As we look towards 2025, both new entrants and experienced participants in the carbon market should focus on:

- Long-term portfolio strategies: Develop approaches that balance risk and impact over multi-year horizons.

- Removal credit investment: Incorporate high-quality removal credits as a core component of a diversified portfolio rather earlier than later.

- Internal capacity building: Strengthen your team's ability to assess credit quality and navigate evolving market standards with the help of technology.

- Foster collaboration: Collaboration is becoming a key piece to climate action. Supporting suppliers with guidance and tooling to co-invest in climate action can unlock additional value quickly.

- Increase adaptability: Maintain flexibility in your strategy to adjust to changing standards and market conditions.

In short: The carbon market is maturing. Quality matters. Buyers are stepping up quietly but effectively. Are you ready to join them? Let’s talk.